CAPM \(\beta\)¶

Regression models a line that might look something like:

Recall that the CAPM equation states:

which we can re-arrange to form:

Note the similarities between this equation and the equation for a straight line. We can use linear regression to fit the re-arranged CAPM equation by writing \(y=R_{i,t}-R_{f,t}\), \(c=0\), and \(x=R_{m,t}-R_{f,t}\). The CAPM formula tells us that the excess return on the stock, \(y\), is equal to the stock’s \(\beta\) times the market risk premium, \(x\), on average. There are random deviations from this average relationship between \(x\) and \(y\), and we model this with the error term \(u\).

The CAPM equation is based on a theoretical relationship between a stock’s excess return and the market risk premium. Per the equation derived by the theory, there is no intercept (equivalently: the intercept is zero).

Below, we will simulate stock return data according to CAPM. Thus, no intercept will be included in the simulated data. After, we will run a regression in statsmodels (which will include an intercept term), and we will see that including an intercept in the regression is actually quite harmless.

Assume that the market return has an average annual return of \(8\%\) and annual volatility of \(10\%\), the risk free rate is constant at \(0.03\), and let \(\beta=1.2\). Simulate one year of returns.

import numpy as np

np.random.seed(0)

annual_mean = .08

annual_vol = .1

annual_rf = .03

mean = (1+annual_mean)**(1/252) - 1

vol = annual_vol / np.sqrt(252)

rf = (1+annual_rf)**(1/252) - 1

mkt_ret = np.random.normal(mean, vol, 252)

mrp = mkt_ret - rf

beta = 1.2

stk_ret = rf + beta * mrp + np.random.normal(0, .005, 252)

excess_ret = stk_ret - rf

Plot the distribution of returns to see what daily returns for the stock look like.

import seaborn as sns

sns.displot(stk_ret, kde=True)

<seaborn.axisgrid.FacetGrid at 0x7fe6e488ce80>

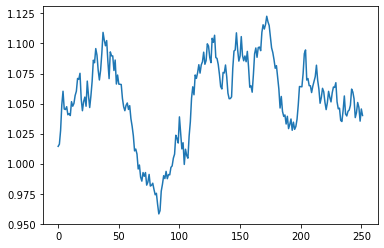

By cumulating the return over the year, we can back out a stock price history for the simulated data.

price = np.cumprod(1+stk_ret)

sns.lineplot(x=range(252), y=price)

<AxesSubplot:>

To run regression on the data, we’ll want to package the return series as a DataFrame. The \(y\) variable is the firm’s excess return and the \(x\) variable is the market risk premium. So, store these two series as columns in a DataFrame.

import pandas as pd

df = pd.DataFrame({'excess_ret': excess_ret, 'mrp': mrp})

df.head()

| excess_ret | mrp | |

|---|---|---|

| 0 | 0.014271 | 0.011301 |

| 1 | 0.001654 | 0.002709 |

| 2 | 0.011082 | 0.006354 |

| 3 | 0.020639 | 0.014304 |

| 4 | 0.010715 | 0.011953 |

Run the regression via statsmodels. By default, an intercept term is included, even though the CAPM equation hypothesizes that the intercept is equal to zero.

import statsmodels.formula.api as smf

mod = smf.ols(formula = 'excess_ret ~ mrp', data=df).fit()

print(mod.summary())

OLS Regression Results

==============================================================================

Dep. Variable: excess_ret R-squared: 0.689

Model: OLS Adj. R-squared: 0.688

Method: Least Squares F-statistic: 554.3

Date: Mon, 06 Dec 2021 Prob (F-statistic): 2.24e-65

Time: 12:11:42 Log-Likelihood: 978.92

No. Observations: 252 AIC: -1954.

Df Residuals: 250 BIC: -1947.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -0.0004 0.000 -1.198 0.232 -0.001 0.000

mrp 1.1835 0.050 23.543 0.000 1.085 1.283

==============================================================================

Omnibus: 0.801 Durbin-Watson: 2.095

Prob(Omnibus): 0.670 Jarque-Bera (JB): 0.555

Skew: -0.092 Prob(JB): 0.758

Kurtosis: 3.139 Cond. No. 160.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Because we simulated data with a zero-intercept, the regression estimates the intercept to be incredibly small.

In the statsmodels.formula.api syntax for regression, the trick to estimating a model without an intercept is to add -1 as a term to the regression. This tells statsmodels to remove the intercept term.

mod2 = smf.ols(formula = 'excess_ret ~ mrp - 1', data=df).fit()

print(mod2.summary())

OLS Regression Results

=======================================================================================

Dep. Variable: excess_ret R-squared (uncentered): 0.687

Model: OLS Adj. R-squared (uncentered): 0.686

Method: Least Squares F-statistic: 551.9

Date: Mon, 06 Dec 2021 Prob (F-statistic): 2.54e-65

Time: 12:11:42 Log-Likelihood: 978.20

No. Observations: 252 AIC: -1954.

Df Residuals: 251 BIC: -1951.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

mrp 1.1798 0.050 23.493 0.000 1.081 1.279

==============================================================================

Omnibus: 0.790 Durbin-Watson: 2.083

Prob(Omnibus): 0.674 Jarque-Bera (JB): 0.548

Skew: -0.092 Prob(JB): 0.760

Kurtosis: 3.135 Cond. No. 1.00

==============================================================================

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors assume that the covariance matrix of the errors is correctly specified.

The \(\beta\) coefficient on the market risk premium is very close to what it was in the model that included an intercept. It’s best to always include an intercept in your regressions. Worst case scenario, the model estimates that intercept to be approximately zero, which tells us that the intercept really isn’t needed. However, in many cases, the intercept is estimated to be non-zero. The fact that CAPM does not include an intercept is due to the theoretical derivation of that model. However, because this model is based on a theory, it may be wrong.